The Peak Has Passed

For a generation, we talked about the demographic cliff the way we talk about retirement: a real thing, definitely coming, comfortably far off. That framing no longer holds. The peak has passed.

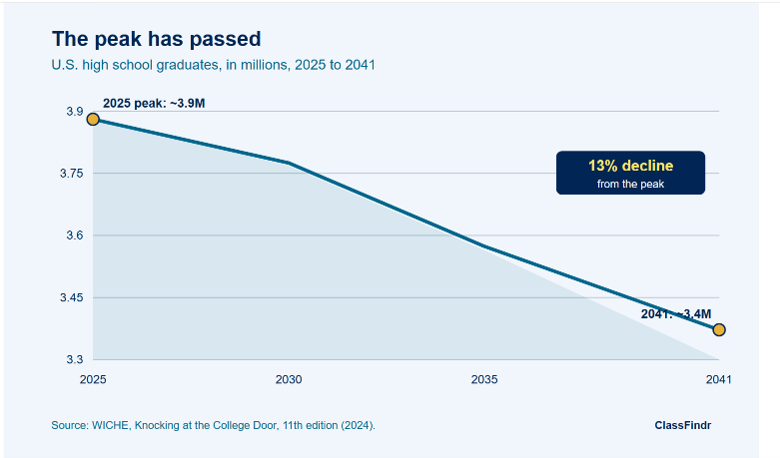

We’re now falling down from the demographic cliff.

The Western Interstate Commission for Higher Education (WICHE) projects that the number of U.S. high school graduates peaked in 2025 at between 3.8 and 3.9 million and will decline steadily through 2041, settling around 3.4 million. That is a 13 percent drop from the peak. The number is not a forecast of something that might happen. It is a description of a pipeline that has already begun to narrow.

Source: WICHE, Knocking at the College Door, 11th edition, 2024.

If you lead an institution, the question on your board’s mind is no longer “is the cliff real.” It is “what is your enrollment strategy for the next decade.” This article is about how to answer that question with something other than more marketing spend.

The Cliff Is Not Evenly Distributed, and That Matters

National averages hide the part that should keep presidents up at night. WICHE projects that 38 states will see fewer high school graduates by 2041 compared to 2023, with the steepest declines concentrated in the Northeast and Midwest. The South is the outlier, with modest growth before a slight decline at the tail end of the projections.

What this means in practice: If your institution draws most of its students from a regional radius in a shrinking state, the cliff is not a 13% problem for you. It’s steeper. Institutions that depend heavily on local, traditional-age enrollment in the hardest-hit regions face the most pressure, and they face it first.

The consequences are already visible. At least 84 colleges have closed, merged, or announced plans to do so since 2020, most of them smaller, tuition-dependent institutions that could not rebuild enrollment.

It is not corruption or mismanagement in most cases. These institutions simply could not bring enrollment back.

A senior policy analyst at the State Higher Education Executive Officers Association put the cause plainly in reporting by The Hechinger Report: It is not corruption or mismanagement in most cases. These institutions simply could not bring enrollment back.

Most Institutional Responses to Declining Enrollment Are Off the Mark

Here is the uncomfortable part. The default institutional response to enrollment pressure is to compete harder for the same shrinking pool of 18-year-olds. More recruitment travel. Deeper tuition discounts. Bigger marketing budgets. This is the 1995 playbook, and it does not work when the pool itself is contracting, because everyone is running the same play against each other and the total prize is smaller every year.

The institutions that will absorb the cliff are the ones diversifying where their students come from, not just spending more to win a larger slice of a shrinking market. That means treating transfer students, adult learners, and multi-institution learners as core enrollment strategy rather than as a supplemental afterthought.

As of the 2023-2024 academic year, 37.6 million Americans had earned some college credit but no credential, according to the National Student Clearinghouse Research Center.

That population grew by roughly a million people in a single year. A majority are adults between 25 and 44, prime working years when the decision to finish a degree is tied directly to career advancement. These are not hypothetical students. They have already chosen higher education once. Many would return if the path back were not so punishing.

Five Moves to Make Before the Enrollment Crisis Becomes an Emergency

None of these requires major capital investment. All of them are levers a president can pull through strategy and policy rather than through construction.

- Build adult learner and stop-out re-enrollment into the core enrollment plan. With 37.6 million people holding some college and no credential, the returning learner is the most overlooked enrollment pipeline in higher education. The institutions that make it easy to come back, recognize prior credit, and finish efficiently will capture a market their competitors are ignoring.

- Treat transfer credit recognition as enrollment infrastructure. When a transfer student loses a semester of credit at your door, you have created friction at the exact moment you were trying to enroll them. Credit mobility is not a registrar’s housekeeping task. It is a front-door enrollment decision with revenue consequences.

- Audit your enrollment concentration risk. Map where your students actually come from, by state and region, against the WICHE projections for those areas. If your feeder population is in a steep-decline region, you have a clearer mandate and a shorter timeline than the national average suggests. Know your real number, not the headline one.

- Explore collaboration before you are forced into it. Course sharing and cross-institutional enrollment let you fill empty seats and offer breadth you could not staff alone. Consortium models have demonstrated enrollment stability that standalone competitors have not. Collaboration is easier to build from a position of strength than from the edge of crisis.

- Diversify the type of student, not just the volume. A resilient enrollment portfolio draws from traditional-age students, transfers, adult returners, and multi-institution learners. Monoculture enrollment, heavy dependence on one shrinking source, is the specific condition that closed most of the 84 institutions that did not make it.

First-Mover Advantage: Higher Ed Presidents Who Move First Will Define the Next Decade

The demographic cliff is not a surprise, and it is not a death sentence. It is a sorting mechanism. It will separate institutions that diversified their enrollment base early from those that kept running the old play until the math caught up with them.

The data is unusually clear for a strategic question of this size. We know the peak has passed. We know which regions decline fastest. We know there are nearly 38 million adults who already started a degree and stopped. The institutions that act on what we already know, before the pressure becomes an emergency, are the ones that will still be here to serve the students who are coming after the cliff.

The other higher ed presidents in your region are reading the same projections you are. The question is who will make the first move.

Page Durham is Chief Academic Officer at ClassFindr, where she leads academic strategy for a platform built to help students navigate course equivalencies, transfer credit, and academic pathways across institutions. She writes about credit mobility, enrollment strategy, and the future of student-centered higher education.